With a team of insurance, commercial real estate, and transaction professionals totaling more than 250 years of combined experience, LGIS is the pioneer of Commercial Property Loan Insurance (CPLI) for the CRE lending industry.

LGIS Group offers a proven risk transfer and mitigation strategy that can replace or supplement the personal guarantee for borrowers of typical short term, recourse commercial real estate loans. Providing significant capital relief to bankers, this empowers them to increase volume and profitability across their CRE portfolios with a competitive advantage.

LOAN INSURANCE COVERAGE

The top 10% to 40% of qualified loan amounts to reduce lenders exposure to foreclosure losses. A foreclosure loss occurs when a foreclosure net sale proceeds are less than the outstanding balance of the loan with adjustments for deductibles and credits.

ELIGIBLE PROPERTIES

- Product Type: Office, Industrial, Retail, Apartments and Hotel.

- Location or Markets: 1st + 2nd Tier cities – Populations >1 million.

- Equity Requirement: 25% to 40%.

- Borrowers: Partnerships, JV, Corporations, LLC’s, Individuals.

ELIGIBLE LOANS

- Construction, redevelopment, acquisition, refinance or rehabilitation / modification loans.

- Loan Sizes: $5 – $200M.

- Term: < 36 months, co-terminus with underlying loan. Extensions available in 3-6 month increments to allow for matching the loan term.

PREMIUMS & FEES

- Premium: 1.50% – 3.75% of loan amount – due at closing.

- Application Fee: $7,500.

Find out more by downloading our brochure.

UNDERWRITING CRITERIA

To mirror same requirements as any good lender’s requirements, with factors to include:

- Financial Soundness.

- Project Feasibility.

- Location.

- Experience of borrower / management / development team.

- Acceptable lender documentation.

- Acceptable lender qualifications – to service and administer the loan.

LENDER ADVANTAGES

- Stronger credit means stronger loans and timely repayment with certainty in full.

- Superior protection against default loss over borrower guarantees.

- Improves capital base, operating efficiencies, and risk position for the portfolio.

- Capital relief and operating efficiencies lead to increased ROE.

- Lower lending costs and terms offer a quantitative competitive advantage.

- Improves customer relationships and increases deposits (plus LGIS Deposit Program).

- Attract more origination business and earn more servicing fees.

BORROWER ADVANTAGES

- First loss position transferred to LGIS.

- Lower borrowing costs and terms improves returns and offsets costs.

- Upgrades lender selection and ability to participate in more deals with no capacity issues.

- Circumvent possible bankruptcy and taxation on debt forgiveness.

- Do more deals!

ADVANTAGES FOR MORTGAGE BROKERS, INSURANCE BROKERS AND CONSULTANTS / OTHERS

- New structural advantage while arranging for short term loans.

- Lift transaction volume and revenue by resolving a key lending issue.

- Improve ability to stay with a client from initial financing through permanent financing / sale.

- Resolves personal guarantee hurdle and help more experienced borrowers qualify.

- Ability to utilize value-add product.

- Consultants can optimize portfolios.

- Do more deals!

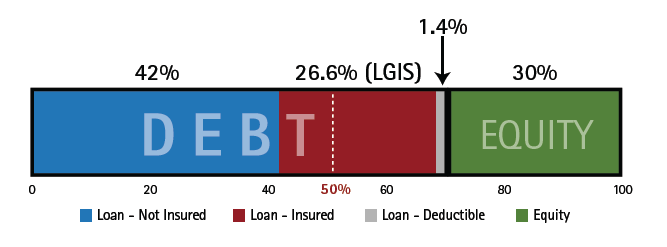

Capitalization Stack Example:

The example below illustrates the capitalization stack for:

- 30% Equity / 70% Loan

- 40% Loan Insurance (% of total loan amount)

- 2% Deductible (% of total loan amount)

Customer Benefit Analysis

EXAMPLE #1

Compare Bank + LGIS v. Alternative Non-Recourse Lender

EXAMPLE #3

Improves Borrowing Terms Analysis

EXAMPLE #2

Default Loss Mitigation Analysis

EXAMPLE #4

Capital Relief Analysis